Whether you’re selling a Craftsman in Ballard or looking to buy a condo in Capitol Hill, choosing the right strategy for transitioning from your current home to a new one can feel overwhelming and lock you in decision paralysis.

Fortunately, multiple proven approaches help you navigate this process smoothly, each with pros and cons. In this blog post, we’ll walk through eight key strategies—from selling your home first or making a contingent offer to more flexible options like renting out your property or using a bridge loan. We’ll explore each strategy's financial risks, loan complexities, potential costs, and ease of moving, providing a comprehensive comparison. By the end, you’ll have access to a powerful decision-making tool to easily compare and customize these options based on your unique financial situation and priorities. Whether your goal is minimizing stress, maximizing profit, or ensuring a seamless transition, this guide will help you make the best choice for your Seattle move.

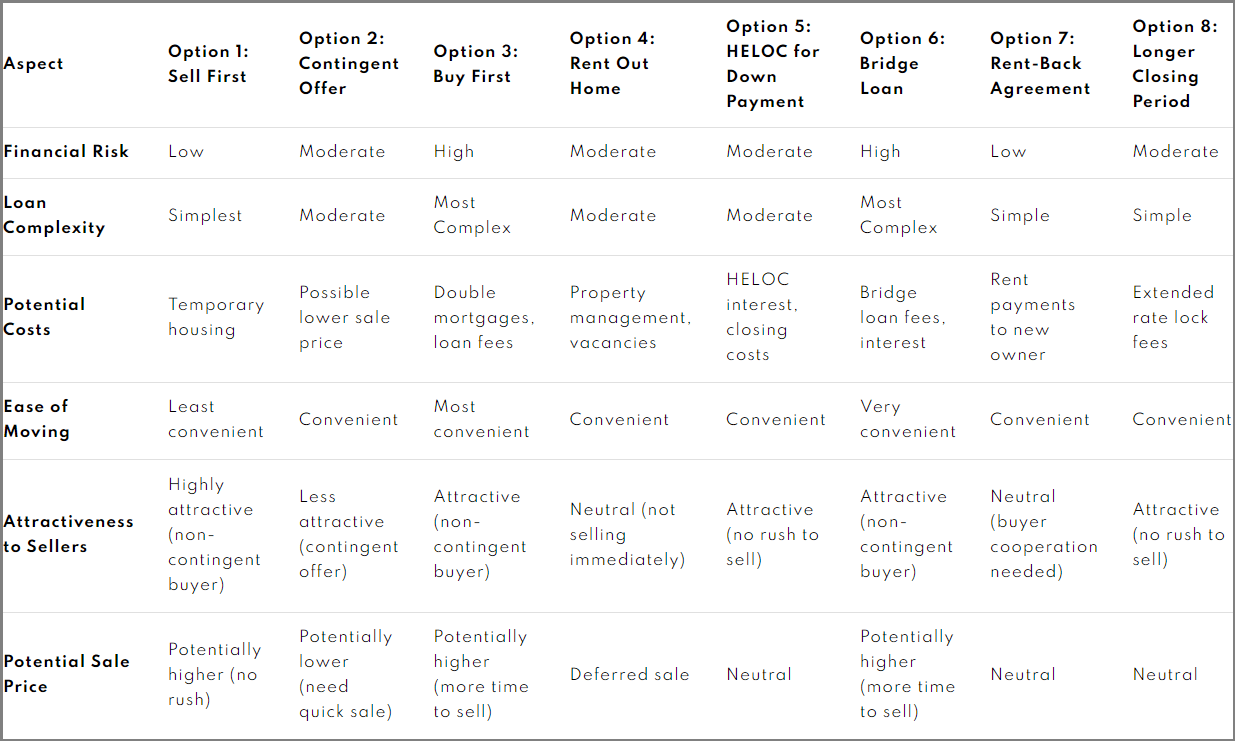

Comparative Summary

1. Sell Your Current Home First, Then Shop for Your New Home

Insight: Selling your current home first in Seattle’s market, where properties can sell quickly, can have the lowest financial risk. This strategy works well in neighborhoods like Ballard or Capitol Hill, where demand is high.

Pros:

- Financial certainty with no overlapping mortgages.

- Stronger buyer position with a potentially more significant down payment.

Cons:

- Living in a home that needs to be photo-ready for tours the entire time it's on the market.

- Occupied homes limit showing availability and may deter buyers.

- Temporary housing needs between selling and buying.

- Pressure to find a new home quickly, especially in fast-moving markets like Seattle.

Ease of Moving:

- Least convenient, as it can require moving twice (into temporary housing and then into your new home) if you cannot find and close your new home before you need to be out of your current one.

2. Make a Contingent Offer on a New Home, Then List Your Current Home for Sale

Insight: In competitive Seattle areas like Queen Anne or West Seattle, contingent offers are often less appealing to sellers, especially if multiple offers are expected. However, this option can still work in less competitive neighborhoods or during the off-season with fewer buyers.

Pros:

- Single move from your old home to the new one; no temporary housing needed.

- Financial flexibility by only buying if your current home sells.

Cons:

- Contingent offers are less attractive to sellers, particularly in Seattle’s highly competitive neighborhoods. This means you may need to offer more for the home you want.

- Sale contingencies typically include a clause that require you to list your home quickly once you're under contract, sometimes in as little as seven days from mutual acceptance.

- Risk of losing the new home if your current one doesn’t sell within the contingency period. This may create pressure to accept less money for your current home to sell quickly.

Ease of Moving:

- More convenient than the first option, with a single move into the new home.

3. Buy a New Home First, Then Sell Your Current Home

Insight: This strategy is popular in the Seattle market, where inventory can be tight. If you’ve found your dream home in Green Lake or Fremont, securing it before selling your current home could be worth the financial strain of holding two mortgages temporarily. This tends to be popular because vacant and staged homes sell fastest and for the highest price compared to other methods. For example, if you can sell a $850,000 home for 3-5% more ($25,500-$42,500), it may make sense to carry two mortgages for a couple of months while your home is on the market.

Pros:

- Maximum convenience, allowing you to move at your own pace.

- Flexibility in selling your current home, giving you time to prepare and market it effectively.

Cons:

- Financial strain from holding two mortgages is a significant challenge in Seattle, where home prices continue to rise.

- Loan qualification challenges due to a higher debt-to-income ratio.

Ease of Moving:

- Most convenient, you can move directly into your new home without time constraints.

4. Rent Out Your Current Home Instead of Selling

Insight: Given Seattle’s strong rental market, especially in high-demand neighborhoods like Capitol Hill or Wallingford, renting out your home could be a viable investment. With high rental demand, this option could generate steady income, but it comes with the responsibility of being a landlord.

Pros:

- Generates rental income, which can help offset mortgage payments.

- Retains ownership, allowing you to benefit from future property appreciation.

Cons:

- Managing tenants and maintaining the property can be time-consuming.

- Financing challenges for a second mortgage, as debt-to-income ratios may be higher.

Ease of Moving:

- Convenient, as you can move into your new home on your timeline.

5. Use a Home Equity Line of Credit (HELOC) for the Down Payment

Insight: If you’ve built significant equity in your home, especially in areas like Magnolia or Ravenna, tapping into it via a HELOC can help you finance a new home purchase without immediately selling your current one. Seattle’s rapidly appreciating market makes this a flexible option.

Pros:

- Access to the equity in your current home to fund your down payment.

- Flexibility in withdrawal and repayment options.

Cons:

- Increases your overall debt load, and interest rates can fluctuate.

- Risk of foreclosure if the HELOC isn’t repaid.

Ease of Moving:

- Convenient, as you can secure a new home without rushing to sell your current one.

6. Bridge Loan

Insight: With home prices in Seattle still rising, a bridge loan can provide the short-term liquidity you need to buy a new home in competitive areas like Laurelhurst or Madison Park before selling your current property.

Pros:

- Provides short-term financing to buy your new home before selling the current one.

- Strengthens your position as a non-contingent buyer in competitive neighborhoods.

Cons:

- Higher interest rates and fees than traditional loans.

- Financial risk if your current home doesn’t sell quickly.

Ease of Moving:

- Very convenient, allowing for a single move into your new home.

7. Sell Your Home with a Rent-Back Agreement

Insight: In neighborhoods like Ballard or Phinney Ridge, where homes are in high demand, a rent-back agreement could give you the time you need to find your next home without rushing out of your current one.

Pros:

- You can sell your home and live in it for a specified period after closing, giving you time to find a new home.

- Eliminates the need for temporary housing and reduces pressure to move immediately.

Cons:

- You may have to pay rent to the new owner during the rent-back period.

- Rent-back periods are short-term, usually lasting 30-60 days, limiting flexibility.

Ease of Moving:

- Convenient, as it allows you to move directly from your old home to the new one.

8. Negotiate a Longer Closing Period

Insight: A longer closing period can be helpful when selling in neighborhoods where buyers are motivated but willing to negotiate, such as in the quieter parts of West Seattle or the Central District. This gives you more time to search for your new home while securing the sale.

Pros:

- Gives you more time to find your new home before the sale of your current one closes.

- Provides flexibility to handle unexpected delays in the moving process.

Cons:

- Some buyers may not agree to an extended closing period, especially in competitive markets.

- Prolonged closing periods could lead to financial uncertainty with interest rate changes.

Ease of Moving:

- Convenient, allowing for a coordinated move without needing temporary housing.

Making the Best Decision for You

It's tough to strike a balance with all the different factors. This is where our comprehensive decision-making tool comes in. We’ve developed a spreadsheet model to help you analyze each approach based on your financial situation and priorities. This tool simplifies decision-making by allowing you to input your financial details and see which option works best for you.

How the Spreadsheet Works:

- Input Your Data:

Enter your current home value, mortgage balance, credit score, and income on the 'Input Data' and 'Assumptions & Calculations' tab. Fill in the cells highlighted in blue. Do not enter data in the yellow highlighted cells. The spreadsheet automatically calculates key metrics like home equity and your debt-to-income ratio. - Set Your Priorities:

Rank the importance of factors such as minimizing financial risk, ease of moving, and maximizing the sale price. You can adjust these based on what matters most to you. Avoid giving blanket rankings for each factor, i.e., all 3's or all 4's. Making a solid distinction between the factors will paint a clearer picture of your path. - Analyze the Options:

The spreadsheet calculates scores for each strategy based on critical factors like financial risk, moving convenience, and potential sale price. - Visualize Your Results:

The tool generates a useful bar graph on the "comparison" tab, which allows you to compare your options visually. - Receive Recommendations:

The spreadsheet offers tailored recommendations based on your input. You can revisit the tool as your situation changes, helping you stay on top of market shifts or financial developments.

Using this data-driven tool, you can confidently decide which strategy suits your needs, balancing financial security, ease of moving, and market positioning. Don't hesitate to reach out if you need help with the spreadsheet or have questions about the inputs.

Choose the Strategy That’s Right for You

Navigating the process of selling your current home and buying a new one can be complex, but with the right tools and information, you can make the process much smoother. Whether you prioritize financial security, convenience, or flexibility, our comprehensive analysis and decision-making tool can help you find the strategy that best aligns with your goals. Ready to get started? Download our spreadsheet model today and make the most informed decision for your next move.

Seattle's real estate market moves swiftly, and having the right guidance can help you achieve the best outcome, whether you're selling, buying, or both. If you're ready to get started, please contact me today. I'm here to assist you in finding the best strategy, connecting you with trusted professionals such as lenders and financial advisors, answering specific questions, and, when you're ready, helping you find your next dream home and secure top dollar for your current one.

Disclaimer

The spreadsheet model and information provided in this post is a tool intended for informational purposes only. It does not constitute financial, legal, or real estate advice. We recommend consulting with qualified professionals before making any decisions.